Learning how to buy a house can feel overwhelming. This guide breaks the process into clear, action-oriented steps so you know what to do, when to do it, and what to watch out for. Read this before touring homes or contacting lenders to avoid expensive mistakes and speed up the purchase.

Why this matters and who this is for

Buying a home is usually the largest financial transaction most people make. This guide is for first-time buyers, people returning to the market, and anyone who wants a practical checklist that covers preparation, financing, offers, inspections, closing, and early ownership responsibilities.

Overview: The high-level path

- Confirm readiness: income, reserves, credit

- Set an affordability limit and budget

- Plan down payment and closing costs

- Get mortgage pre-approval

- Assemble your team (agent, lender, inspector)

- Search with clear priorities

- Make offers and negotiate

- Conduct inspections and order appraisal

- Negotiate repairs, credits or price adjustments

- Final walkthrough and close

- Plan for post-closing maintenance and costs

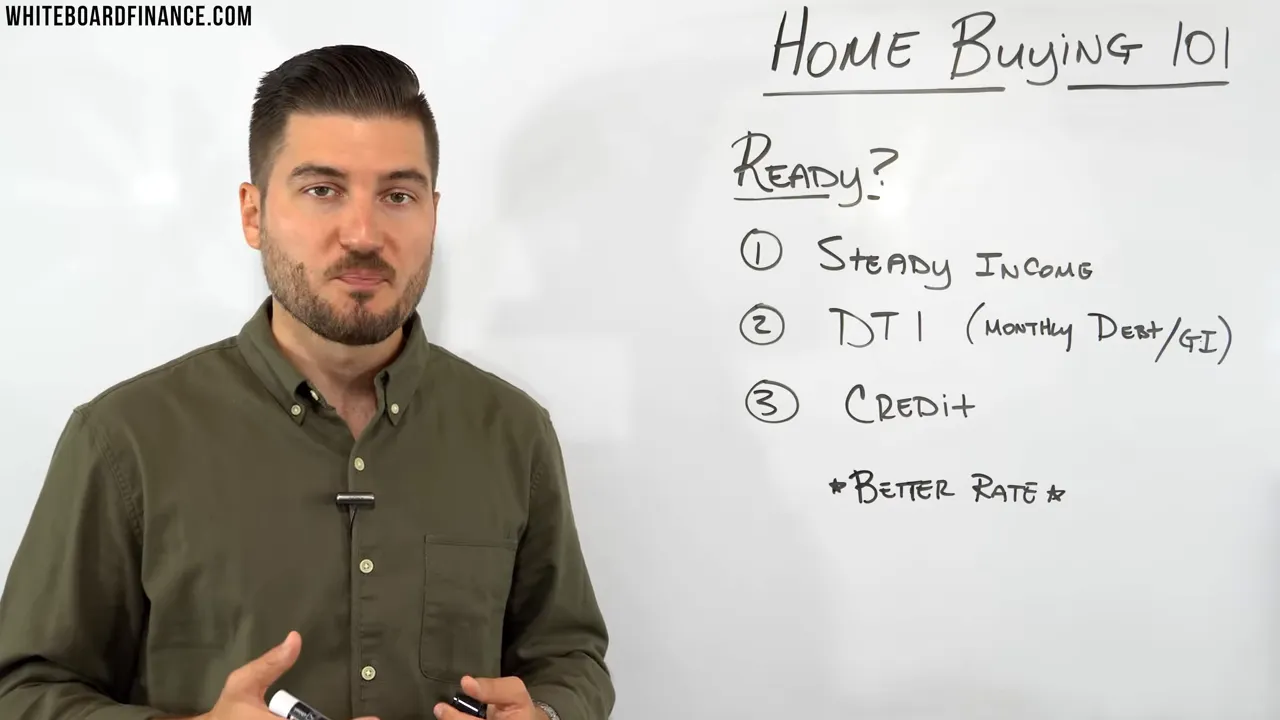

Step 1 — Are you ready to buy?

Before committing, evaluate three fundamentals:

- Income stability: Lenders prefer steady pay. If your income fluctuates, target at least six to twelve months of living expenses in reserves.

- Debt-to-income ratio (DTI): Lenders calculate DTI using gross income. Aim to keep total monthly debt payments under about 36% of gross pay. Lower is better for rate and approval odds.

- Credit score: Better scores unlock lower mortgage rates. Check your reports for errors and correct them before applying.

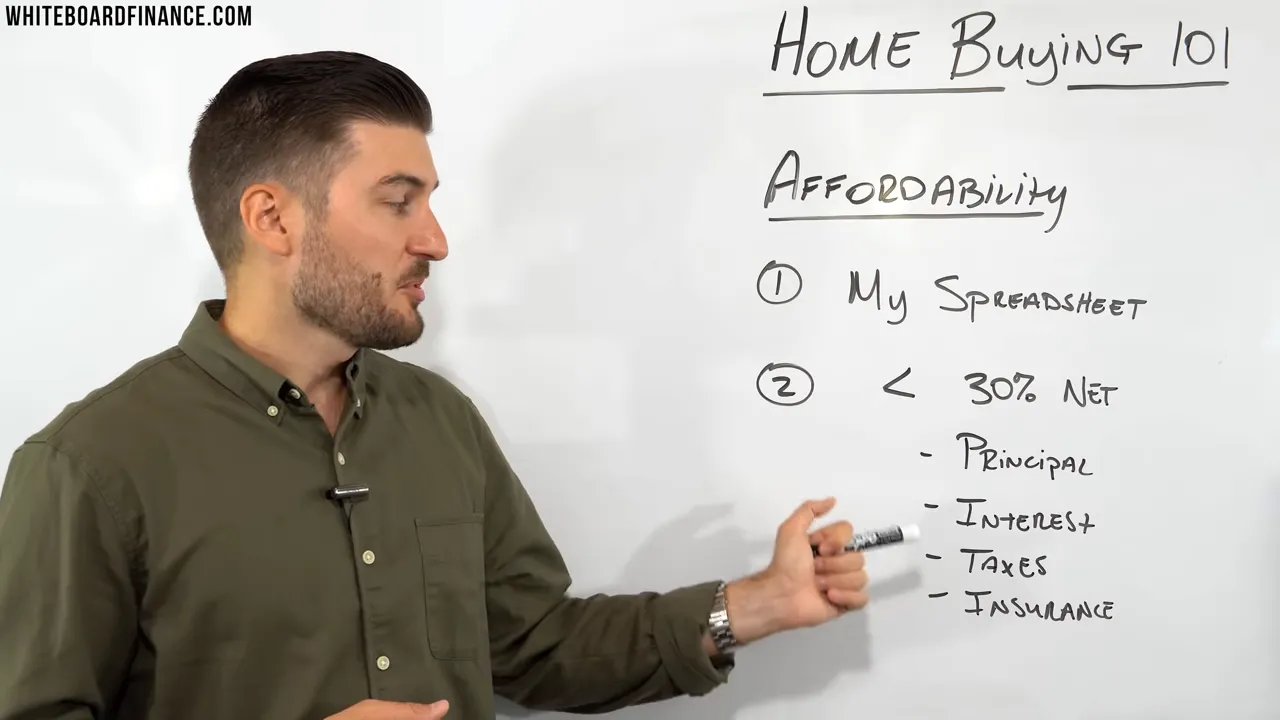

Step 2 — Figure out how much house you can afford

Knowing how much home you can comfortably afford prevents becoming "house poor." Use a conservative rule: spend no more than 30% of your net (take-home) income on total housing costs (mortgage principal and interest, property taxes, insurance, HOA fees and utilities).

Simple monthly example:

- Net pay: $6,000 per month

- 30% limit for housing: $1,800 per month

- Estimate mortgage payment, taxes, insurance and HOA to see the price range that matches $1,800.

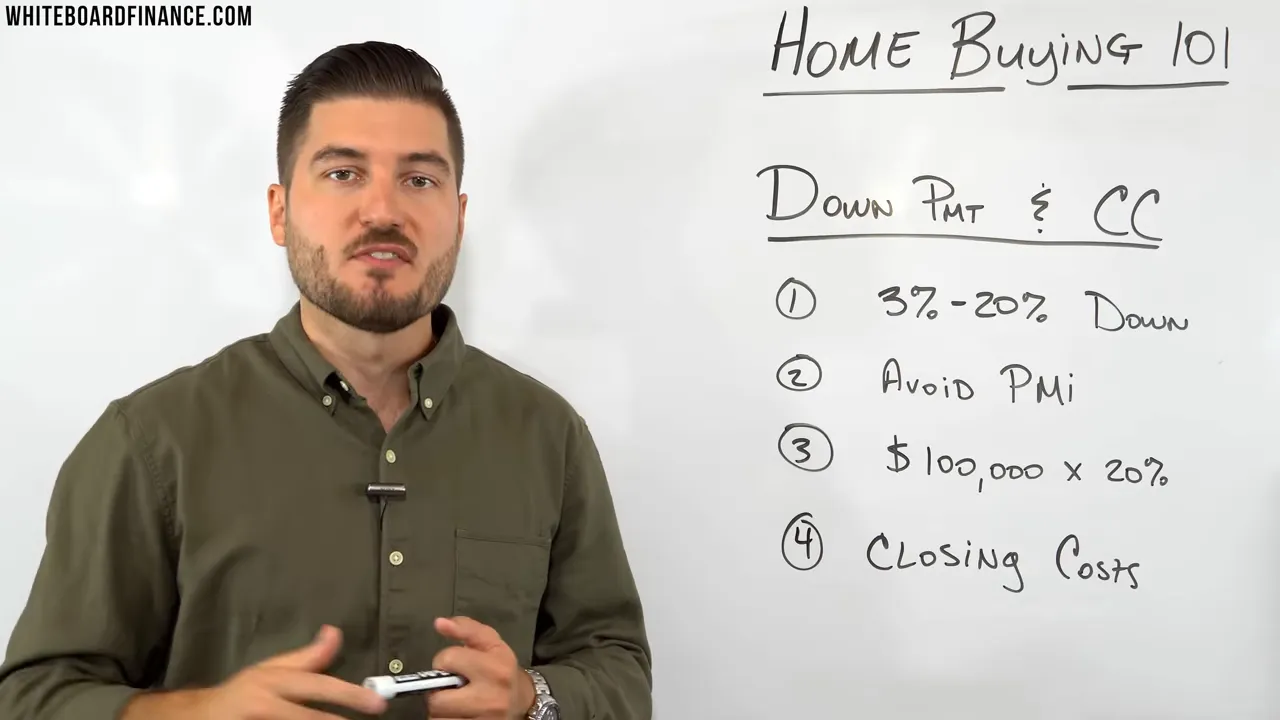

Step 3 — Down payment and closing costs: plan the cash needed

Two cash items you must plan for:

- Down payment: Typically 3%–20% for many conventional loans. Putting at least 20% avoids private mortgage insurance (PMI), which is an added monthly cost that protects the lender.

- Closing costs: Fees for appraisal, title, loan origination and more. Expect roughly 1%–6% of the purchase price; setting aside about 3% is a useful rule of thumb.

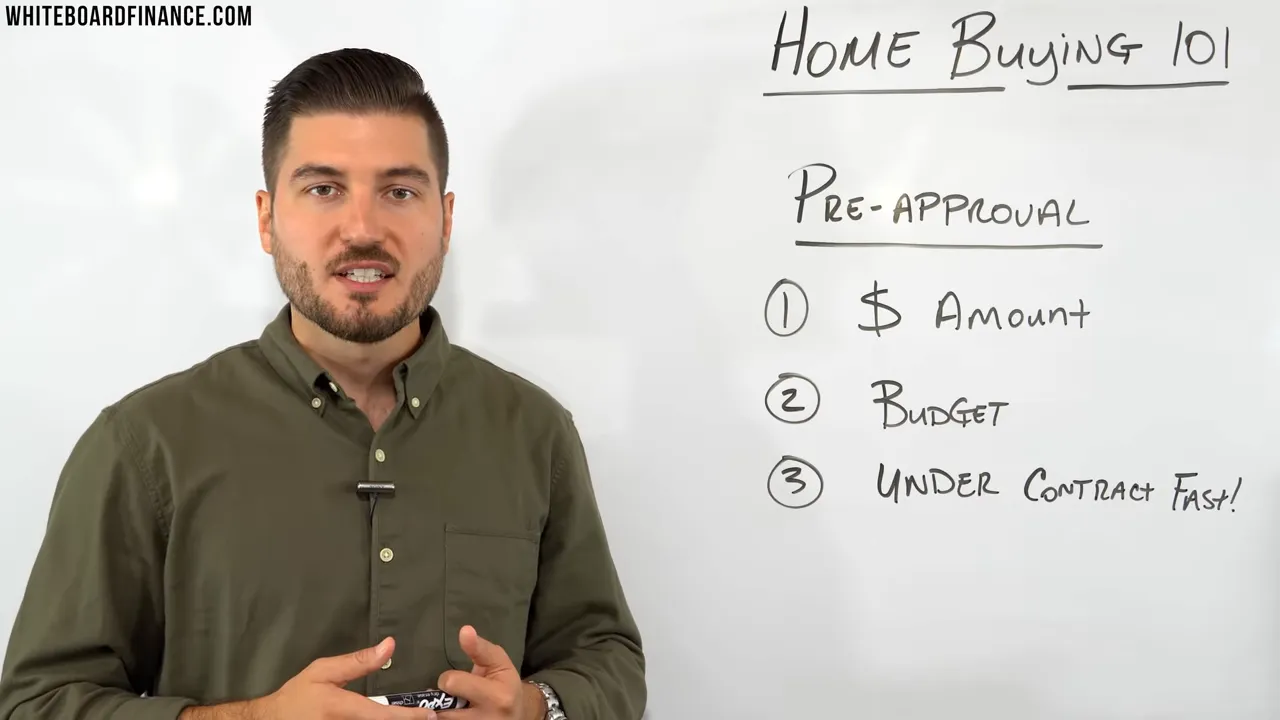

Step 4 — Get pre-approved for a mortgage

A mortgage pre-approval is a written estimate from a lender stating how much they are willing to lend based on your financial documents. It helps in two ways:

- It narrows your price range so you search efficiently.

- It strengthens offers because sellers see you have lender backing.

Provide pay stubs, W-2s, bank statements and ID. Avoid big purchases or new credit applications between pre-approval and closing.

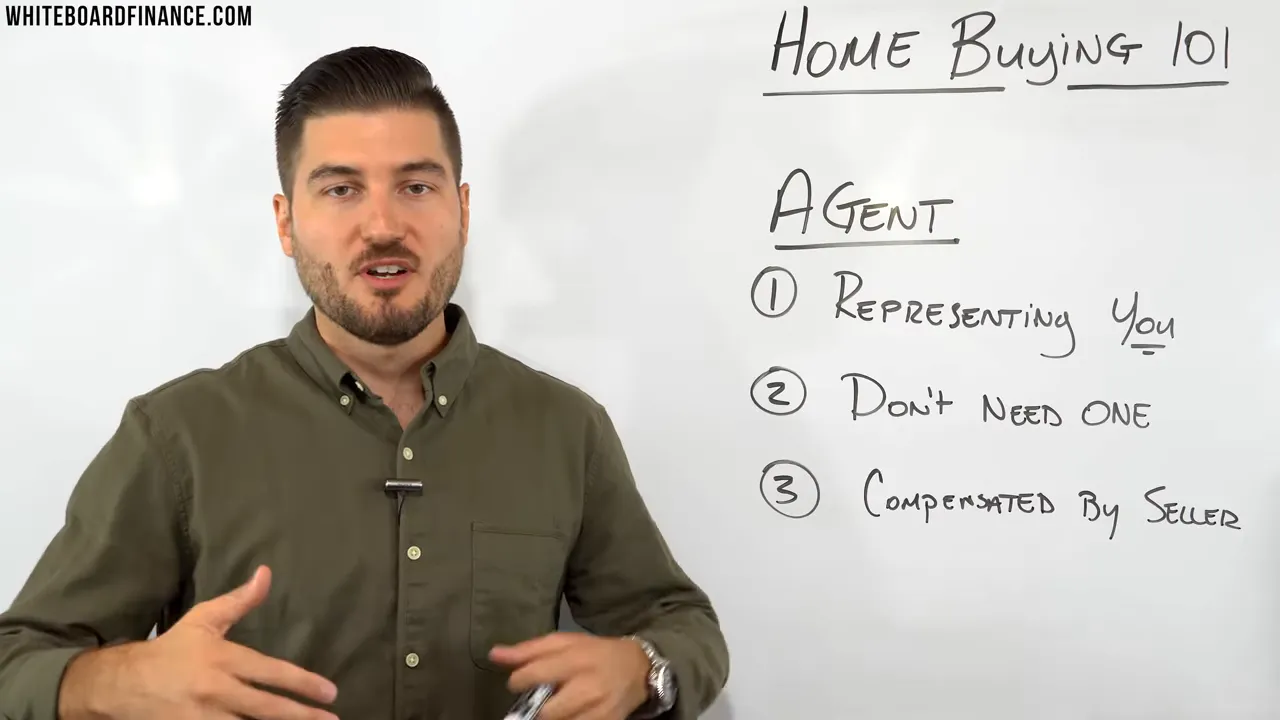

Step 5 — Build your buying team

The core professionals are:

- Buyer's agent: Represents your interests during the search and negotiation. Agents are typically paid from the seller’s commission, but clarify compensation and expectations upfront.

- Lender/mortgage officer: Shop several lenders to compare rates, fees and service. Ask about lock periods and rate lock costs.

- Home inspector: Finds hidden problems after your offer is accepted.

- Title company and real estate attorney: Handle paperwork and clear title issues.

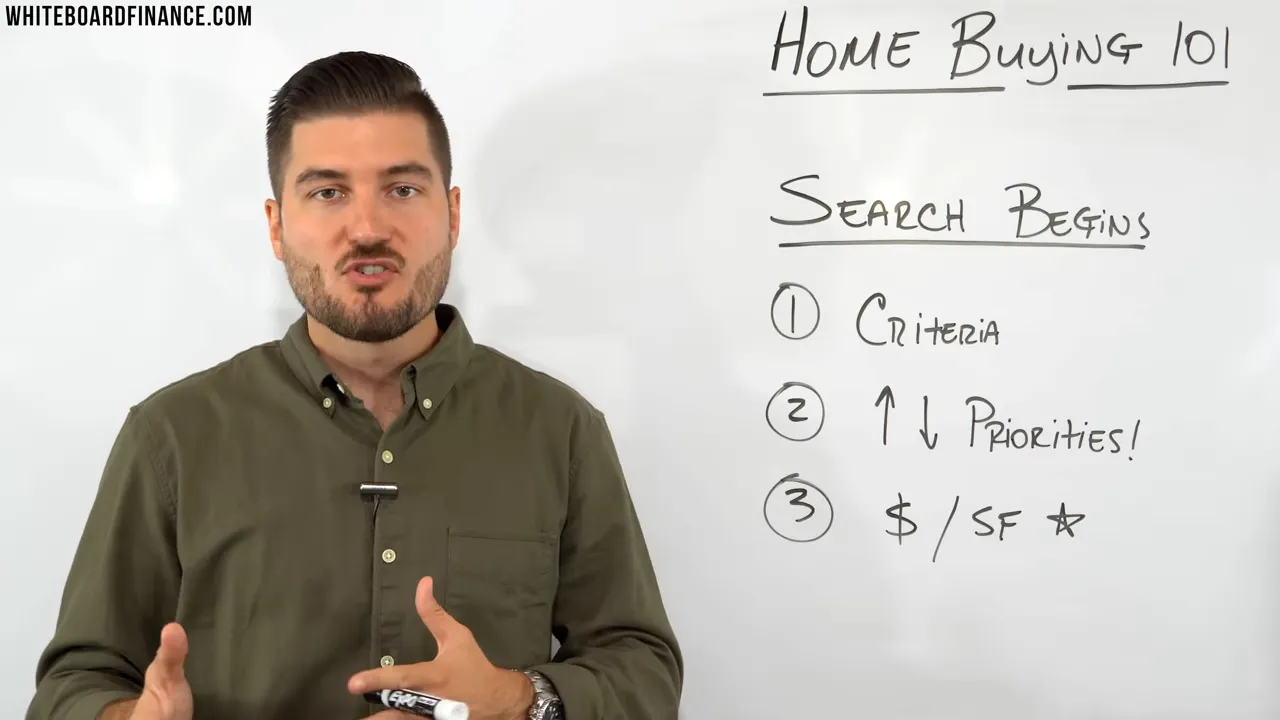

Step 6 — Search with clear priorities

Create a prioritized list of needs versus wants. Rank items (location, school district, commuting time, number of bedrooms, yard size, pool, garage, etc.) from essential to optional. This saves time and reduces emotional decisions.

Use price per square foot to compare similar properties and spot outliers. If two homes have similar features but one costs substantially more per square foot, investigate why before overpaying.

Step 7 — Making an offer and negotiating

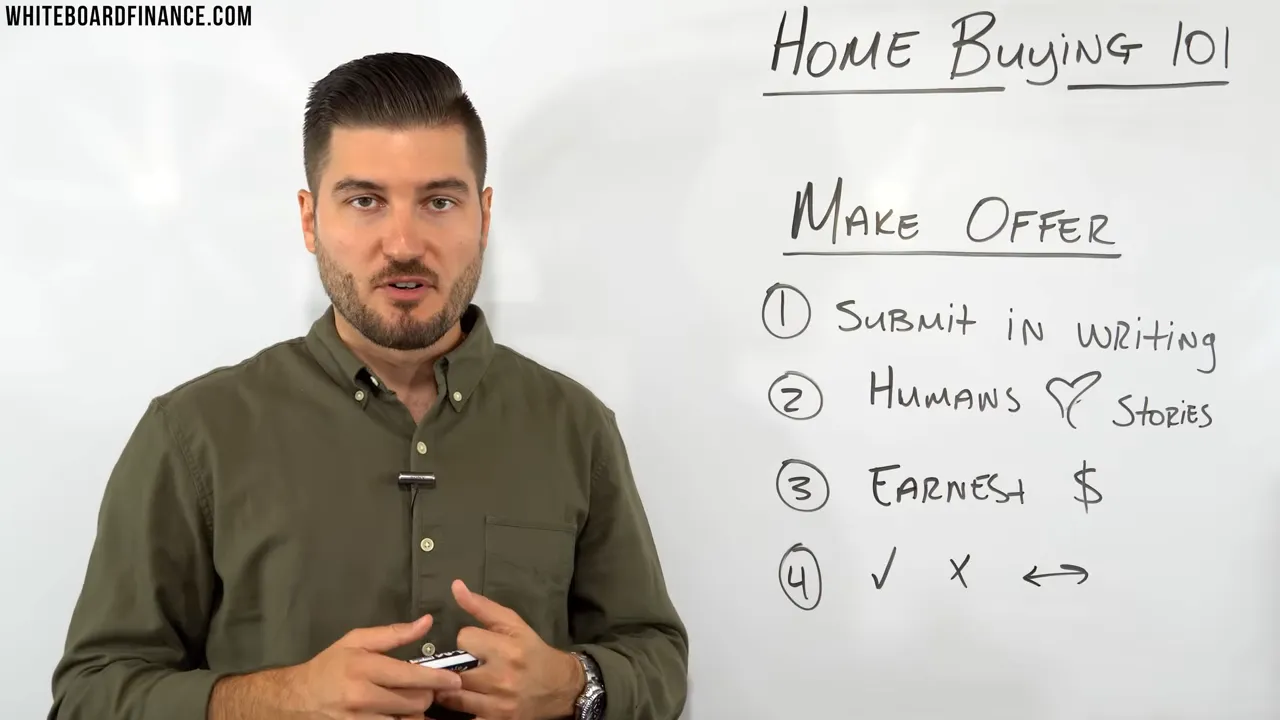

When you find a home you like, the offer packet typically includes price, contingencies, proposed closing date and earnest money. Key points:

- Earnest money: A deposit showing good faith. It goes toward closing or can be forfeited if you back out for reasons outside agreed contingencies.

- Contingencies: Typical contingencies include financing, inspection, appraisal and title. They protect you—don’t remove them lightly, especially in a first purchase.

- Offer strategy: In a competitive market, strong pre-approval, flexible closing timelines, and reasonable earnest money help. In some cases a personal letter (brief and sincere) can sway a seller who values the buyer's story, but never rely on this instead of a strong financial offer.

Step 8 — Inspection and appraisal after contract

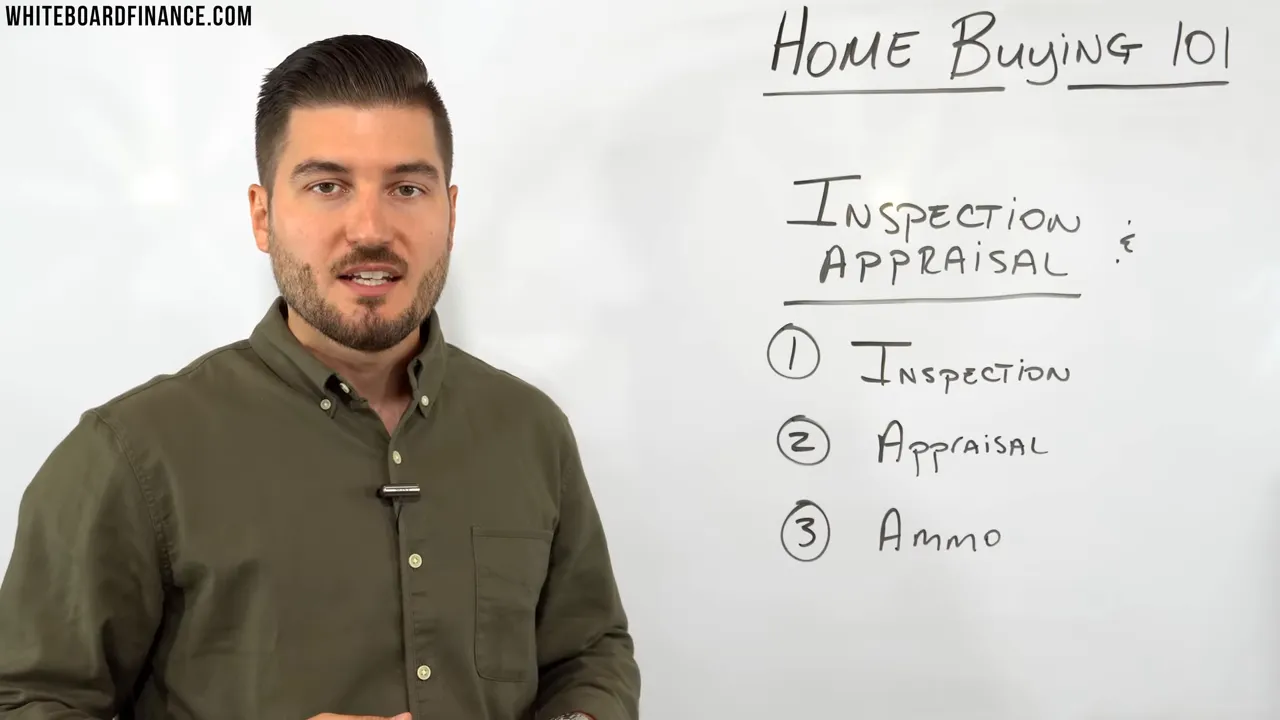

After the seller accepts your offer and you’re under contract, schedule:

- Home inspection: A qualified inspector checks structure, roof, HVAC, plumbing, electrical, mold, radon and other issues. Use the inspection report to decide on repairs or credits.

- Appraisal: Lender-ordered valuation based on comparable sales. If the appraisal comes in lower than the purchase price, you’ll need to cover the gap, renegotiate, or the lender may not approve the loan amount.

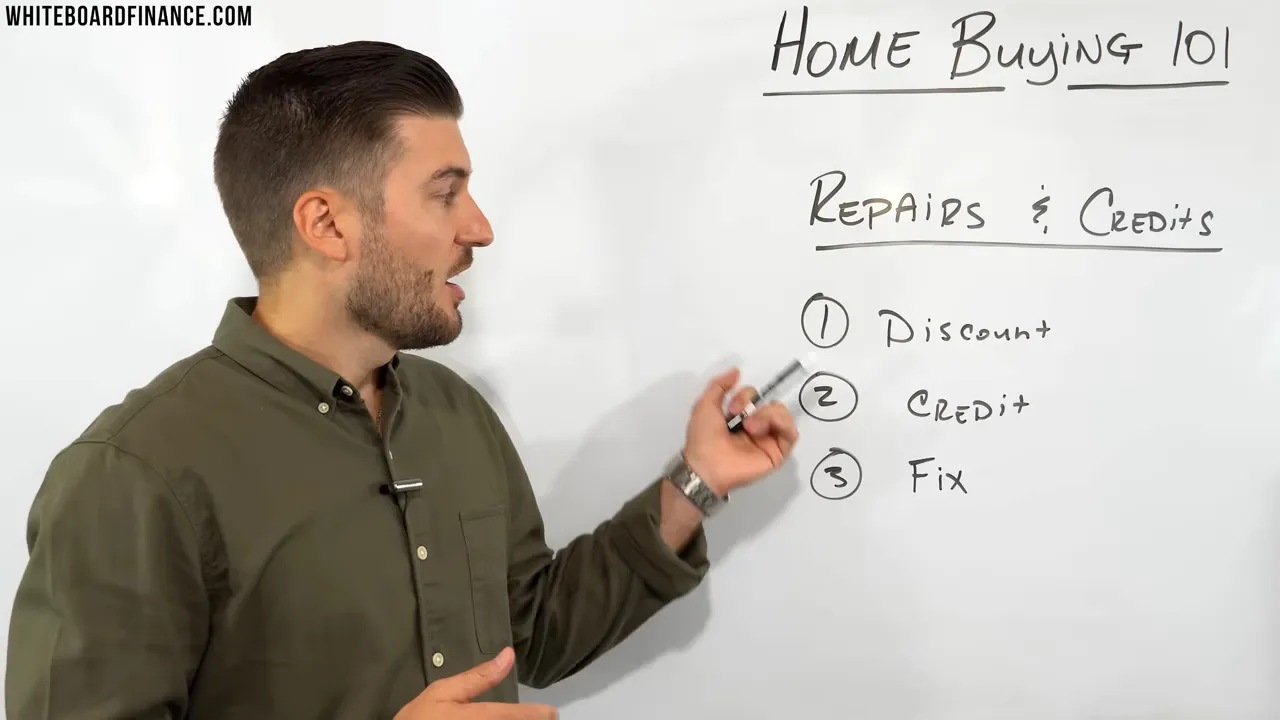

Step 9 — Negotiating repairs, credits and contingency resolutions

Use inspection and appraisal results as leverage:

- Ask the seller to complete repairs before closing.

- Request a credit at closing so you can manage repairs yourself after possession.

- Negotiate a lower purchase price if major defects or a low appraisal appear.

Keep negotiations focused on cost estimates and objective reports rather than emotions.

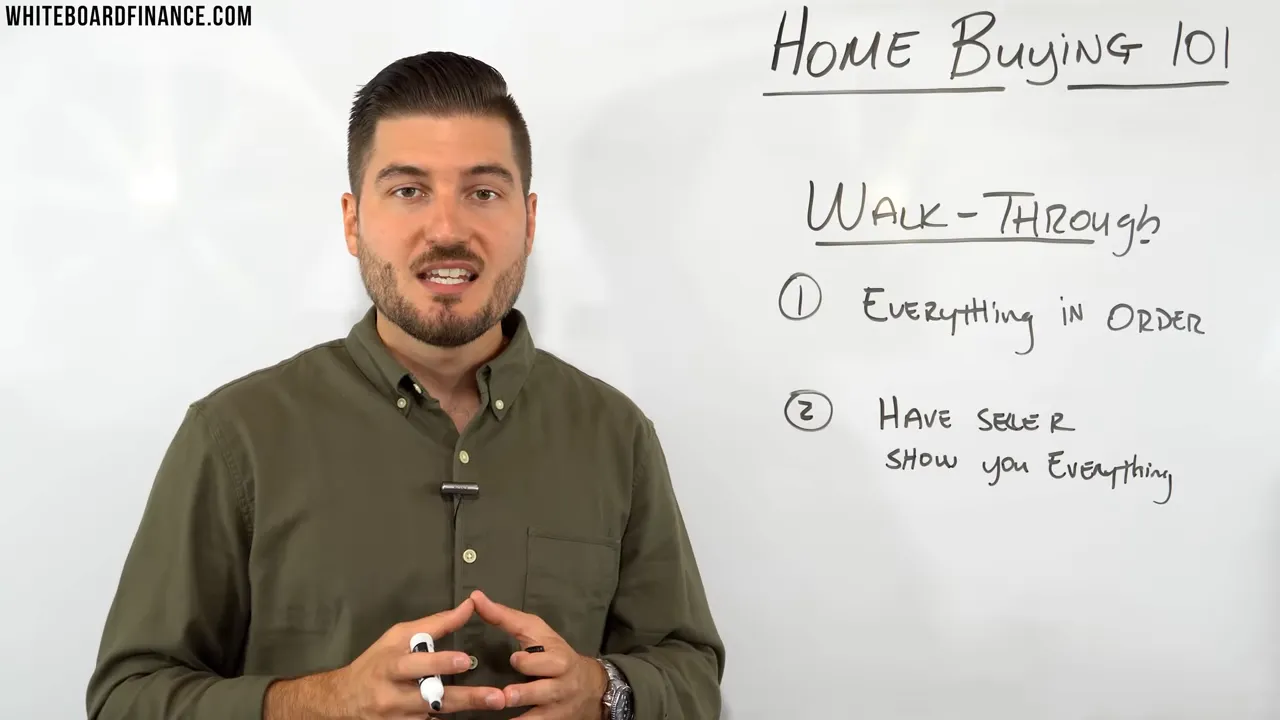

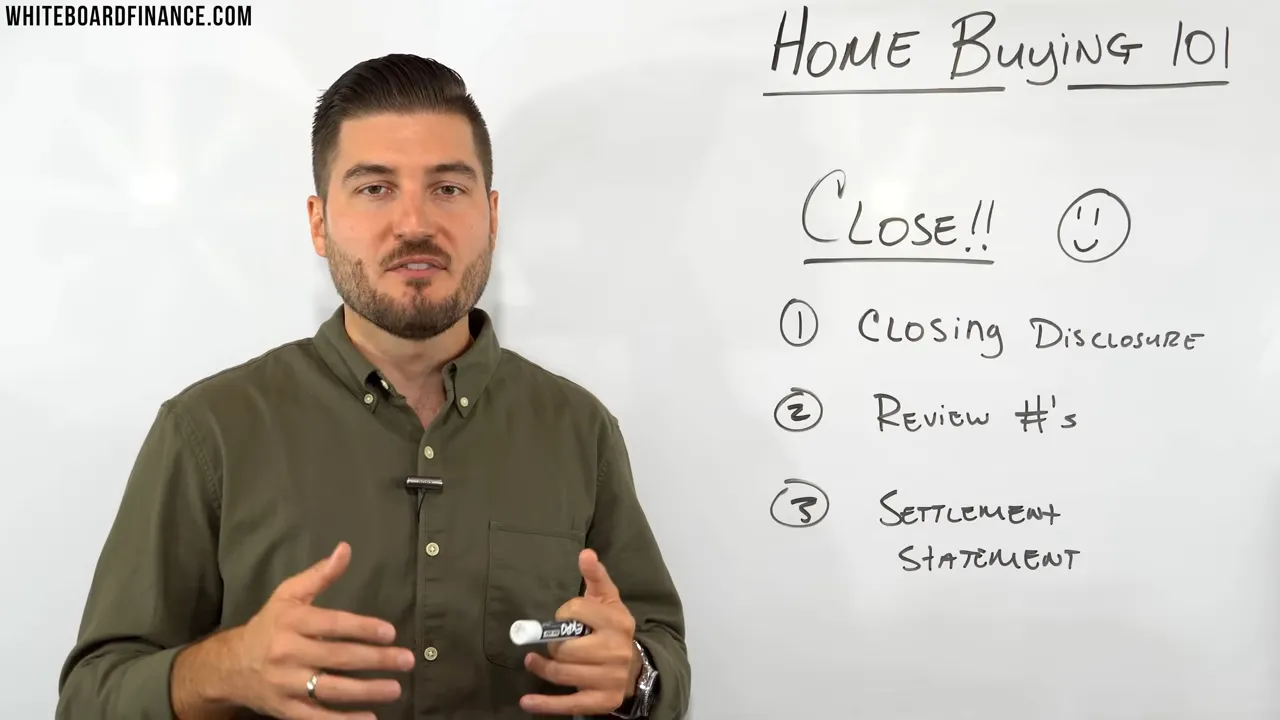

Step 10 — Final walkthrough and closing

The final walkthrough (usually 24–72 hours before closing) confirms the property’s condition matches the contract:

- Check that agreed repairs were completed.

- Confirm nothing the seller agreed to leave behind was removed.

- Document new damage with photos and contact your agent immediately if issues appear.

At closing bring required funds and photo ID. Review the closing disclosure and settlement statement carefully; confirm totals, prorations and that the mortgage terms match what you expected.

Step 11 — After closing: budgeting for ownership

Homeownership brings ongoing costs. Budget for:

- Maintenance and repairs (plan 1%–3% of the home value annually)

- Property taxes and homeowner’s insurance (can change yearly)

- Utilities, HOA fees and unexpected replacements (HVAC, roof)

Build an emergency fund for major repairs and set aside a small monthly amount for routine upkeep.

Common mistakes and how to avoid them

- Overextending on price: Use the 30% net housing guideline to avoid being house poor.

- Skipping inspection: A cheap inspection can uncover thousands in repairs; budget for it.

- Not shopping lenders: Rates and fees vary. Compare at least three lenders for the best total cost.

- Making large financial changes during underwriting: Don’t open new lines of credit, change jobs, or make big purchases before closing.

- Underfunding closing and reserves: Keep reserves even after closing; moving-in costs and initial repairs add up.

Quick checklist: Before you make an offer

- Mortgage pre-approval in hand

- Maximum monthly housing budget set (30% of net income)

- Down payment and closing funds available

- Buyer's agent selected and communication plan set

- Priority list for features and must-haves

- Contingency strategy decided (inspection, financing, appraisal)

Short FAQ: People also ask

How much should I put down when buying a house?

Minimums vary by loan type. Conventional loans often start at 3% down, but putting 20% avoids PMI and lowers total monthly cost. Use your situation and market conditions to decide.

What is earnest money and how much is typical?

Earnest money is a good-faith deposit that accompanies an offer. Typical amounts range from a few hundred to several thousand dollars depending on price and local custom. It is applied toward closing costs or down payment if the sale completes.

What is the difference between an inspection and an appraisal?

An inspection evaluates condition and needed repairs. An appraisal estimates market value for the lender. Both are critical—inspection for condition, appraisal for financing.

Final takeaways

Learning how to buy a house becomes manageable when you break it into preparation, financing, team selection, disciplined searching, careful negotiation, and prudent post-closing planning. Prioritize affordability, protect yourself with contingencies, and budget for ongoing maintenance. With the right preparation you can move from renter to confident homeowner without avoidable surprises.

Buyer's final checklist (printable)

- Pre-approval letter

- Proof of down payment funds

- Budget set with 30% net housing limit

- Agent and lender contacts

- Inspection scheduled after contract

- Closing disclosure reviewed 3 days before closing

- Emergency fund for first-year ownership