If you are preparing to move to Dubai, one of the first “real life” tasks is getting a bank account set up. It sounds simple, but the UAE banking process has a few details that can trip you up, especially if you need a current account and a checkbook soon.

This guide breaks down what to prepare, which banks are commonly recommended, how to think about account types, and why your signature consistency matters a lot when using checks.

Which banks to consider in Dubai

There are many banks in the UAE, and it helps to start with a shortlist. A practical approach is to use more than one bank for different purposes, depending on where you live and what products you need (everyday spending, savings interest, credit cards, and so on).

Popular options mentioned: Emirates NBD, Mashreq, and Mashreq’s alternatives

One common recommendation is to focus on these banks and their setups:

- Emirates NBD: A large, well-established bank with many branches.

- Mashreq (often described as having branches “almost every corner” in Dubai): Two main account options are commonly discussed:

- Mashreq Neo (standard product)

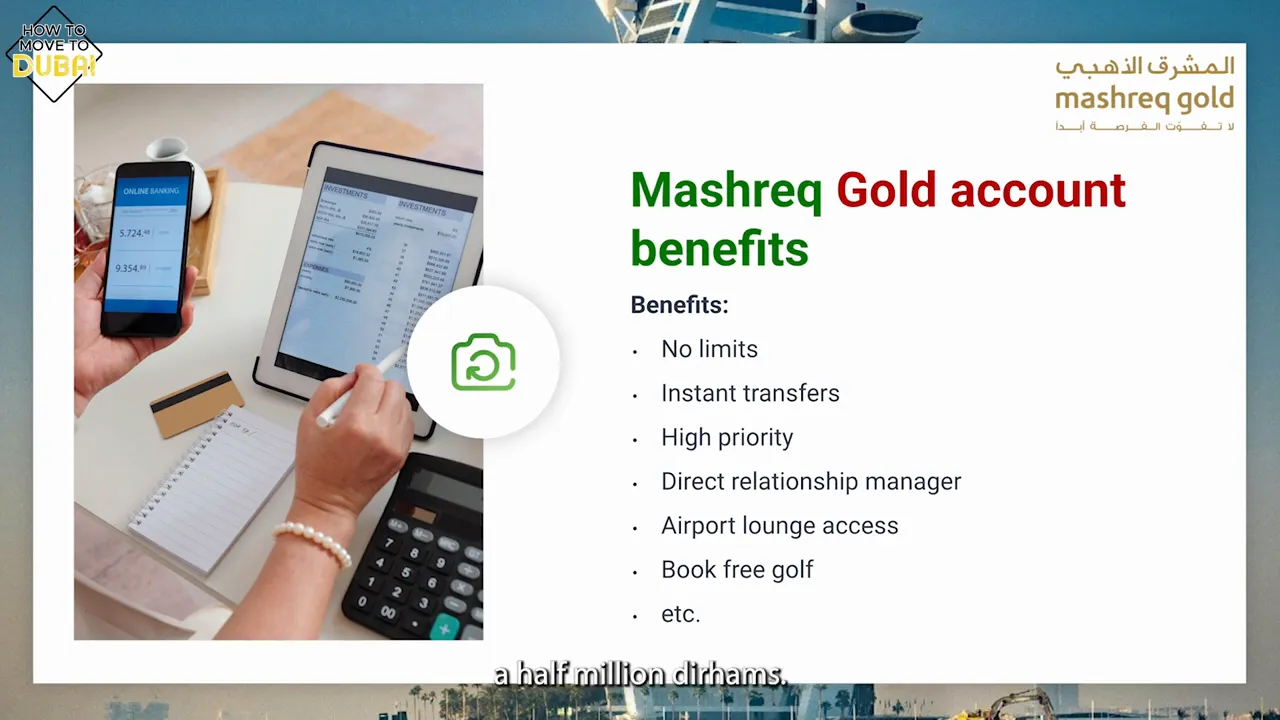

- Mashreq Gold (a higher-tier option)

Another bank often used in parallel is Vio (also referenced as part of a multi-bank strategy for different needs).

If you are curious about digital options, a future option mentioned is Revolut, described as a digital bank today, potentially expanding with more UAE presence and physical services like branch support and checkbooks in the future.

Tiered accounts: Mashreq Neo vs Mashreq Gold (what changes?)

With Mashreq, the application process and banking system are described as similar across account types, but there can be benefits with a higher-tier product if you meet the requirements.

Mashreq Gold: the typical minimum fund requirement

The commonly remembered guideline is a minimum of about 500,000 AED (noted as “half a million dhams”). That can be in:

- Liquidity (money sitting in your account)

- Assets (for example, bonds or similar holdings)

The practical benefit described is a more premium experience, including an example of VIP or fast-lane service inside the branch (a “Gold line” versus a “normal customer line”).

Think beyond the account: credit cards can be useful (if you can manage them)

Many UAE banks offer credit cards, and credit cards can be dangerous for people who do not manage spending carefully. But if you can handle them responsibly, they can also be beneficial.

Example: Skywards earning through a credit card

One example mentioned is a Skywards card tied to Emirates, allowing you to earn miles when you use the card. If your spending is predictable and you pay attention to balances and due dates, points or miles can add up.

Don’t choose blindly: check the current interest rates

Before selecting a bank, it is smart to compare current savings account interest rates. These rates can change, but the guidance is clear: research it first, even if you already know the bank brands.

An example rate mentioned was around 5.3% interest on a savings account at the time of reference.

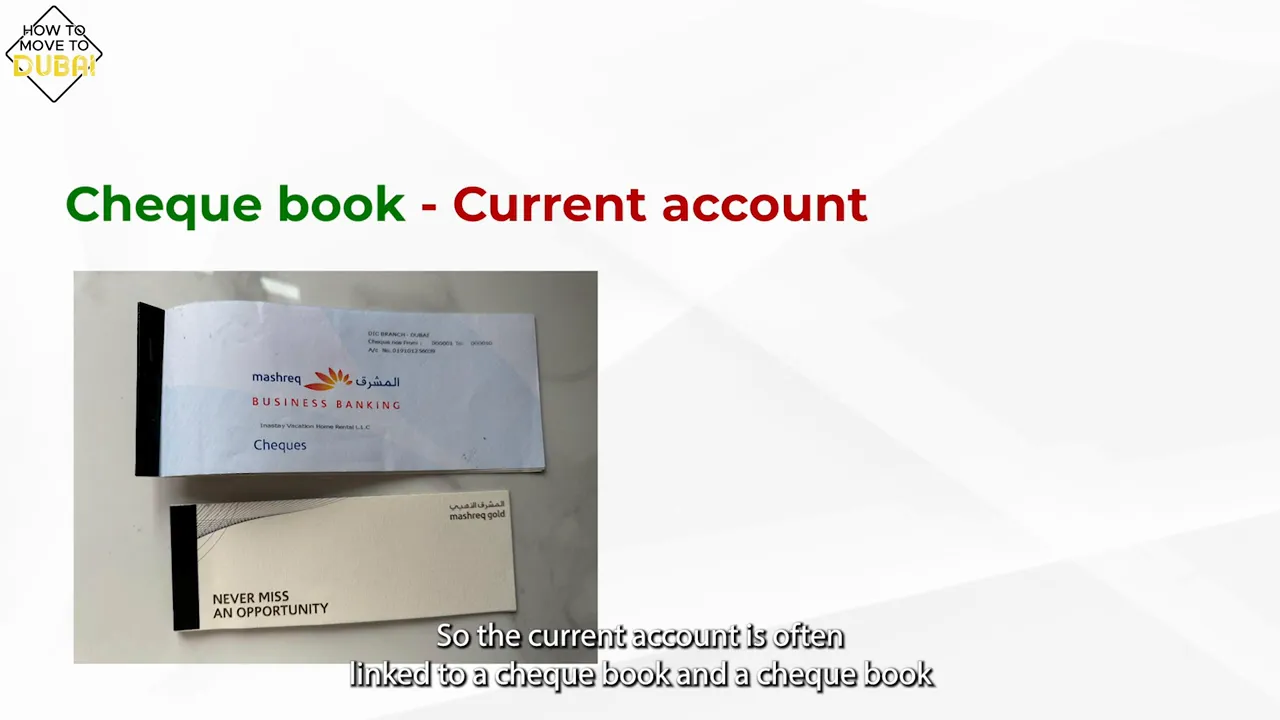

Account type matters: you usually need a current account for a checkbook

One key point for Dubai specifically: you will likely need a checkbook at some stage. For example, it becomes especially useful when renting or buying property.

When opening your account, make sure you open a current account.

Why current account is important

The reason is simple: a checkbook is often linked to a current account. If you select another account type, it is not guaranteed that you can get checkbooks.

Checks can look unfamiliar if you come from a place where they are less common, but they are still very normal in the Dubai real estate and payments ecosystem.

Checkbook and signature: the “one-line difference” problem that causes bounced checks

This is the part people often do not think about until it becomes stressful.

When writing checks, you must use your signature consistently. A common mistake is signing slightly differently each time. If the new signature does not match the signature on file, the payment can bounce and the recipient may not receive the money.

Practical advice

- Use a signature that matches what the bank has on record (often connected to how you signed during account setup and as per your passport signature).

- Practice the exact signing style because even a small change can be enough to cause issues.

In short: your signature is not just paperwork. It is part of the payment system integrity.

How to open bank account Dubai: do it yourself (documents first, then the branch)

You can find consultancy firms that offer “help” to open an account, but it is described as pretty straightforward to do it on your own.

A common method described is simply going to a branch, preparing everything, and getting the account details on the spot (including things like your account number).

Documents you typically need to open a bank account

The biggest success factor is readiness. Before going to a branch or applying online, prepare your documents.

Core requirements

- Emirates ID (the most important document)

- Visa (and often your passport as well)

- UAE phone number

- Bank statements from your current bank (if you have an account abroad)

- Proof of address

If you do not have your final address yet

A realistic scenario: when the bank asked for address proof, the person referenced did not yet have a new home and was staying on an Airbnb (short-term and not a long-term lease). The bank reportedly said it was okay for now and that the details could be updated later.

So if your situation is similar, don’t panic. Just be transparent and provide what you have.

Employment documentation (if requested)

- If you are employed: salary and employment documentation (such as payslips)

- If you are self-employed: it may involve trade license or other documentation

KYC is ongoing: update it every year or face freezes

All banks in the UAE must follow KYC rules, meaning Know Your Customer. The important part is that KYC is not only a one-time step.

What to expect

- You can expect to update KYC annually.

- Banks often request this via email.

- If you ignore it, you can receive warnings and, in the end, your account can be frozen until you complete the update.

Actionable tip: treat bank emails seriously. This is one of those “small things” that can create a big headache later.

Shared or joint accounts: family-only in most cases

If you want to share an account with someone else, note the restriction described: a shared account is generally allowed if you are:

- Married, or

- Blood related

Sharing with a friend or non-family partner is typically not allowed. Joint accounts with business partners are described as possible only under specific setups and family-related conditions.

Financing later: why local banks often want UAE salary for loans

Once your account is open, many people also start exploring financing options: personal loans, car loans, and home loans.

Here is the practical reality described: local banks typically require that you can prove you receive a salary from a UAE company. If your salary is from your home country or from abroad, local banks may not accept it for loan approvals.

Payslip history requirements

- Often banks ask for at least six months of payslips (sometimes three months, but six is common)

Self-employed applicants: approvals can be difficult

It is also mentioned that self-employed people may struggle significantly with approvals, especially when new in Dubai. The “sad news” shared is that many self-employed clients end up needing to pay for major purchases in cash, such as a car, because loan approval becomes very hard.

Home financing can also be challenging because banks value job stability and pay slips as security. Even if you can show payslips from your own company, the risk profile can be treated as higher.

Mortgage details are noted as something to cover later in the larger course structure (Model 7, section 7.6), meaning financing strategies are deeper than just opening a bank account.

Quick checklist: How to Open Bank Account Dubai

- Choose the right account type: aim for a current account if you need a checkbook.

- Compare interest rates on savings accounts before deciding.

- Prepare your documents:

- Emirates ID

- Visa and usually passport

- UAE phone number

- Bank statements (if requested)

- Proof of address

- Employment documents if needed

- Expect KYC updates annually and respond to bank emails.

- When using checks, keep your signature consistent with the one on record.

If you follow these steps, opening and using a bank account in Dubai becomes much more predictable, and you will avoid the most common “surprises” people run into when they are new to the system.

")